How Property Condition Shapes Insurance Claim Valuation

Property condition is the single most consequential factor in insurance claim valuation, determining how insurers calculate depreciation, adjust market value, and set final payout amounts. The industry term for this process is “condition-based valuation,” and it sits at the intersection of physical inspection, depreciation methodology, and market evidence. Whether you are an insurance adjuster working a residential loss or a property owner disputing an actual cash value (ACV) estimate, the role of property condition in claim valuation directly controls how much money changes hands. Getting it right requires understanding the frameworks, the discount ranges, and the evidence standards that govern every step.

What types of property conditions affect claim valuation?

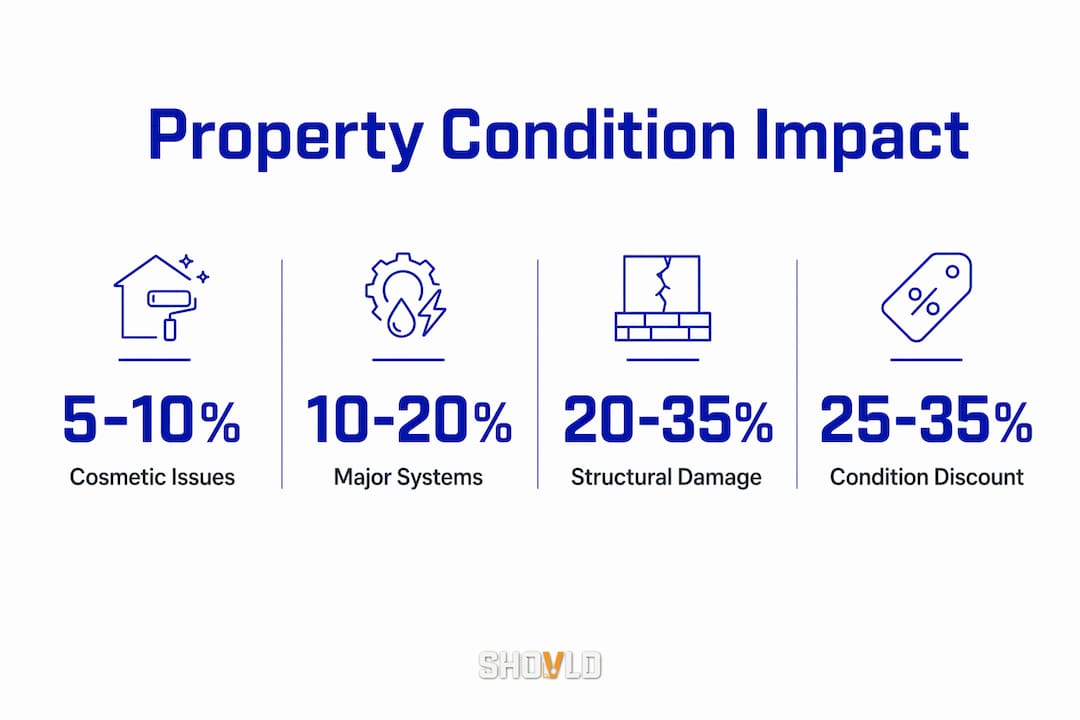

Property condition issues fall into three distinct categories, and each carries a different financial penalty in claim valuations. Cosmetic issues such as worn paint, dated fixtures, and minor surface damage typically reduce value by 5–10%. Major system failures, including HVAC, plumbing, or electrical problems, drive discounts of 10–20%. Structural damage, such as foundation cracks or roof deck deterioration, pushes discounts as high as 20–35%. These ranges are not arbitrary. They reflect what buyers actually pay less for in the open market, and insurers use comparable market behavior to anchor their depreciation decisions.

The financial stakes are significant. A property with a replacement cost of $400,000 and documented structural damage could see its ACV reduced by $80,000–$140,000 based on condition alone. That gap is the difference between a claim that covers a full rebuild and one that leaves the owner funding repairs out of pocket.

Condition also affects the financing pool available to buyers, which in turn shapes market value. A property with major system failures cannot qualify for conventional mortgage financing in many cases. That restriction shrinks the buyer pool, which appraisers and adjusters must account for when establishing pre-loss market value.

Pro Tip: Document every property system separately. Roof, HVAC, plumbing, and electrical each carry their own depreciation schedule. A well-maintained HVAC on a property with a worn roof should not drag down the HVAC’s effective age in the claim.

How condition categories translate to claim discounts

Condition CategoryTypical Discount RangeCommon ExamplesCosmetic issues5–10%Worn paint, dated flooring, minor fixturesMajor system failures10–20%HVAC failure, outdated electrical, plumbing leaksStructural damage20–35%Foundation issues, roof deck damage, load-bearing wall damage

How do adjusters incorporate condition into claim valuation methods?

Insurance adjusters use two primary tools to account for property condition: depreciation schedules and the broad evidence rule. Depreciation schedules assign a default useful life to each property component. A roof might carry a 20-year useful life. If the roof is 10 years old, the adjuster applies 50% depreciation to its replacement cost. The problem is that default schedules ignore actual condition. A 10-year-old roof that has been professionally maintained and never leaked is not the same as one that has been neglected for the same period.

The broad evidence rule corrects for this by requiring adjusters to consider all relevant evidence, including maintenance history, pre-loss appraisals, inspection reports, and photographs, rather than relying solely on age-based formulas. States including Florida, New York, and Texas have adopted this standard. It gives adjusters the legal authority to override default depreciation when the evidence supports a different effective age.

Valuation software like Xactimate provides a starting point for claim calculations, but it defaults to average depreciation unless the adjuster manually overrides the effective age. That default setting penalizes well-maintained properties. An adjuster who accepts the software output without reviewing condition evidence is not doing a complete job.

Physical deficiencies that affect safety, soundness, or structural integrity must appear in appraisal reports because they materially impact valuation and claim outcomes. Adjusters who skip this step expose their employers to disputes and litigation.

The practical workflow for a thorough condition-based valuation looks like this:

Conduct a physical inspection and assign a condition rating to each major system.

Collect maintenance records, service logs, and pre-loss inspection reports.

Review photographic evidence from before the loss event.

Compare the property’s effective age against its chronological age for each component.

Apply broad evidence rule overrides where documented condition differs from default depreciation assumptions.

Support any condition adjustment with paired sales data or regression analysis from the local market.

Pro Tip: When reviewing a claim, request the property’s permit history. Permitted improvements, such as a roof replacement or electrical upgrade, are public record and directly support a lower effective age for that component.

What steps help owners and adjusters get accurate condition-based valuations?

Active evidence collection is the most critical step to disputing unjust depreciation. Policyholders who accept ACV estimates without challenge often leave significant money on the table. The same principle applies to adjusters who want defensible valuations that hold up in appraisal or litigation.

For property owners, the documentation checklist is straightforward:

Maintenance records: Service invoices, warranty documents, and contractor receipts for every major system.

Pre-loss photos: Dated photographs of the roof, HVAC, foundation, and interior finishes taken before any damage event.

Professional appraisals: A licensed appraiser’s opinion of pre-loss value carries significant weight in disputes.

Contractor estimates: Repair bids from licensed contractors establish current replacement costs and condition baselines.

Permit history: Pulled permits document when systems were replaced or upgraded, directly supporting effective age arguments.

Condition adjustments in appraisal reports must be supported by market evidence such as paired sales or regression analyses to be defensible. An adjuster or appraiser who writes a 15% condition adjustment without market support will lose that argument in a dispute. Paired sales analysis compares two similar properties where the only meaningful difference is condition, then measures the price gap. That gap becomes the market-supported adjustment.

Successful condition-based property tax appeals demonstrate how powerful this evidence can be. Documented condition evidence can save homeowners $1–$3 per square foot annually in tax assessments. The same documentation that wins a tax appeal also strengthens an insurance claim.

Pro Tip: Build your property condition file before you ever need it. A folder with dated photos, service records, and permit copies takes an afternoon to assemble and can shift a claim outcome by tens of thousands of dollars.

Platforms like Shovld track distressed property indicators and public-record signals that reveal deferred maintenance patterns across markets. For adjusters and restoration professionals, that signal data provides early visibility into properties where condition documentation is likely to be contested.

How has the 2026 market widened the gap between property conditions?

The 2026 real estate market has made condition more financially consequential than at any point in the past decade. Buyer hypersensitivity to defects and deferred maintenance has widened the price gap between well-maintained and dated properties. Appraisers are now applying larger condition adjustments than in previous years because the market data demands it. When buyers consistently pay less for properties with deferred maintenance, appraisers must reflect that in their reports.

“Buyers’ hypersensitivity to deferred maintenance in 2026 creates wider valuation spreads between well-maintained and dated properties, reinforcing the need for precise condition assessments in claims. Adjusters who rely on historical averages are increasingly out of step with what the market actually shows.”

This shift has direct implications for claim valuation. A property that would have received a 10% condition discount in 2022 may now warrant a 15% discount because the market evidence supports a larger gap. For property owners, this means a well-documented pre-loss condition becomes even more valuable. For adjusters, it means market-supported condition adjustments are no longer optional. They are required for defensible valuations.

Market PeriodTypical Condition Adjustment RangeDriverPre-20225–10% for most condition categoriesSeller’s market, buyers accepted more defects202610–35% depending on condition severityBuyer hypersensitivity, tighter financing standards

The practical takeaway is clear. Both adjusters and property owners need more precise condition documentation now than they did three years ago. The market has moved, and claim valuations must move with it.

Key Takeaways

Property condition directly controls claim valuation outcomes, and the evidence you collect before a loss event determines whether the final payout reflects the property’s true pre-loss worth.

PointDetailsCondition drives depreciationStructural damage alone can reduce ACV by 20–35%, making condition the largest single valuation variable.Broad evidence rule mattersStates like Florida, New York, and Texas require adjusters to weigh all condition evidence, not just age-based formulas.Default software undervalues good propertiesXactimate defaults to average depreciation; manual overrides require documented condition evidence to be effective.Market conditions have shifted2026 buyer behavior has widened the price gap between maintained and dated properties, increasing adjustment ranges.Evidence collection is non-negotiableContractor estimates, pre-loss photos, and permit records are the tools that shift claim outcomes in the policyholder’s favor.

Why condition evidence is the argument adjusters and owners keep losing

I have watched both sides of this process make the same mistake repeatedly. Adjusters accept software defaults because it is faster. Property owners accept ACV estimates because they do not know they can push back. The result is a systematic undervaluation of well-maintained properties and an overvaluation of neglected ones.

The broad evidence rule exists precisely because age-based depreciation is a blunt instrument. A 15-year-old roof that has been recoated, inspected annually, and documented with service records is not the same asset as a 15-year-old roof that has never been touched. Treating them identically is not just unfair. It is inaccurate.

The adjusters I respect most treat condition evidence the way a good attorney treats discovery. They collect everything, organize it by component, and build a case before they write a number. The owners who get fair settlements do the same thing. They walk into the process with a folder, not a complaint.

The 2026 market has made this discipline more urgent. Larger condition adjustments mean larger dollar swings. A 5% difference in condition assessment on a $500,000 property is $25,000. That is not a rounding error. It is a meaningful outcome that documentation can control.

My advice is direct: treat your property condition file as a financial asset. Update it annually. Pull permits when you replace systems. Photograph everything. When a claim arrives, you will not be starting from zero. You will be presenting a case.

— Avi

Shovld’s tools for tracking property condition signals

Property condition does not appear out of nowhere. Deferred maintenance, code violations, and permit gaps leave public-record trails long before a claim is filed.

Shovld tracks those signals across U.S. markets, giving adjusters, restoration companies, and public adjusters early visibility into properties where condition documentation is likely to be thin or contested. The platform aggregates permit records, code violations, distressed-property indicators, and deferred maintenance patterns into scored opportunities. For professionals who need to act before a situation becomes crowded, that signal data is a real advantage. Review Shovld’s pricing plans to find the tier that fits your market coverage and workflow needs.

FAQ

What is the role of property condition in claim valuation?

Property condition determines how insurers calculate depreciation and adjust market value when settling a claim. Poor condition reduces the actual cash value payout, while documented good condition supports a higher settlement.

How much can property condition reduce an insurance claim payout?

Cosmetic issues typically reduce value by 5–10%, major system failures by 10–20%, and structural damage by 20–35%. The final impact depends on documented evidence and the valuation method the adjuster applies.

What is the broad evidence rule and how does it affect claims?

The broad evidence rule requires adjusters in states like Florida, New York, and Texas to consider all relevant condition evidence, including maintenance records and pre-loss photos, rather than relying solely on age-based depreciation formulas.

Can a property owner dispute an ACV estimate based on condition?

Yes. Collecting contractor repair estimates, professional appraisals, and pre-loss photographs is the most effective way to challenge default depreciation assumptions and improve a claim outcome.

How does the 2026 market affect condition-based claim valuations?

Buyer hypersensitivity to defects in 2026 has widened the price gap between well-maintained and dated properties. Appraisers are now applying larger condition adjustments, which means accurate pre-loss documentation carries more financial weight than in prior years.