How to Evaluate Distressed Property Investment Value

Evaluating distressed property investment value is defined as the systematic process of determining both the current as-is worth and the realistic after-repaired potential of a property in financial or physical distress. Investors who skip this process buy on hope instead of data. Accurate valuation requires combining a Property Condition Assessment (PCA), a licensed appraisal, and a disciplined underwriting model that accounts for repair reserves, holding costs, and market timing. Get it right, and distressed real estate delivers returns that stabilized assets cannot match. Get it wrong, and the deal destroys capital fast.

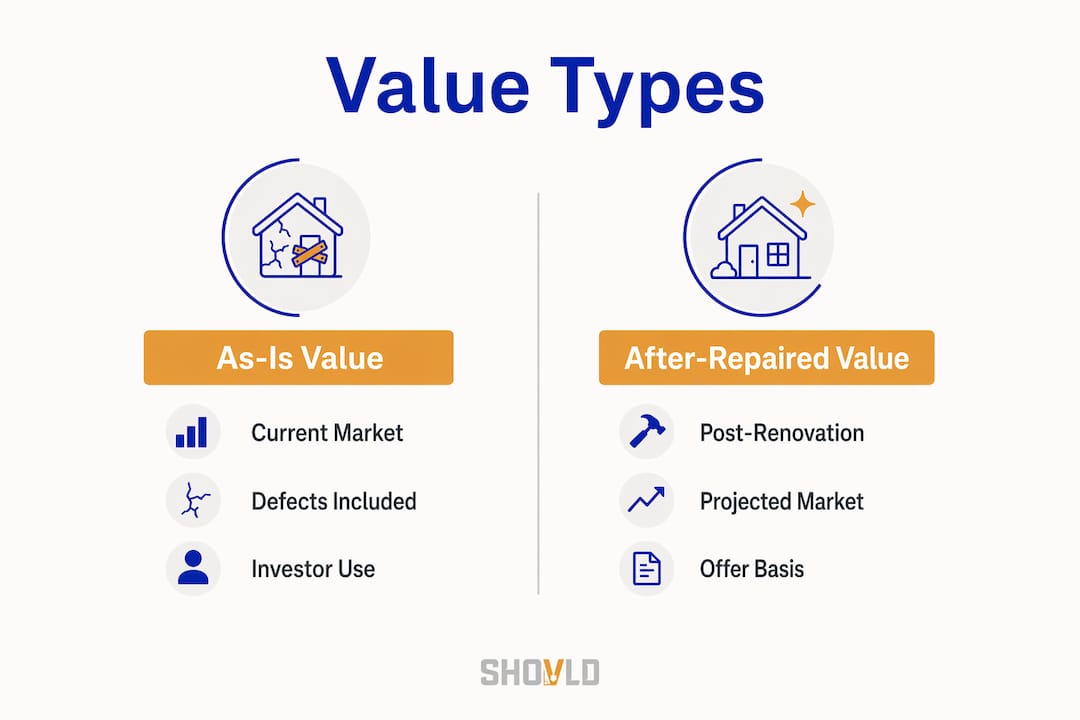

What key property values must investors differentiate when evaluating distressed properties?

The single most important distinction in distressed property appraisal is the gap between As-Is Value and After-Repaired Value (ARV). Investors must strictly differentiate these two figures to avoid deal failure. Confusing them is the most common reason investors overpay.

As-Is Value is what the property is worth today, in its current condition, with all defects, deferred maintenance, and occupancy problems included. ARV is what the property will be worth after all planned repairs and improvements are complete. The spread between these two numbers is where your profit margin lives.

Two other figures create confusion: assessed value and appraised value. They are not interchangeable.

| Value Type | Definition | Investor Relevance |

|---|---|---|

| As-Is Value | Current market worth with all defects | Sets your maximum offer price |

| After-Repaired Value (ARV) | Projected worth post-renovation | Determines exit price and profit ceiling |

| Assessed Value | Government estimate for tax purposes | Unreliable for transaction pricing |

| Appraised Value | Licensed appraiser’s market opinion | Most reliable for financing and offers |

Assessed value often lags market shifts and is an unreliable proxy for current transaction pricing. A property assessed at $180,000 in 2022 may trade at $240,000 or $140,000 in 2026 depending on neighborhood trajectory. Never anchor your offer to the tax record.

The ARV calculation depends entirely on recent comparable sales, called comps, pulled from properties that have already been renovated and sold within the same submarket. Comps older than six months in a shifting market carry real risk. Use the most recent sales within a half-mile radius and adjust for square footage, condition, and amenity differences.

Pro Tip: Run two ARV scenarios: a conservative case using the lowest comparable sale and an optimistic case using the highest. Your offer price should work under the conservative scenario.

How to conduct a property condition assessment for distressed assets

Physical Property Condition Assessments are the backbone of any serious distressed property evaluation. A PCA exposes liabilities that financial records and tax documents cannot reveal. Skipping it is not a shortcut. It is a gamble.

A thorough PCA covers these core areas:

- Structural integrity: Foundation cracks, load-bearing wall damage, and framing issues are the most expensive repairs an investor faces. Hire a licensed structural engineer, not just a general inspector, when any structural concern exists.

- Roof condition: Age, material, and visible damage determine whether you face a repair or a full replacement. A 25-year-old asphalt shingle roof on a distressed property is almost always a replacement cost, not a patch.

- Mechanical systems: HVAC, plumbing, and electrical systems in distressed properties are frequently deferred or damaged. Disconnected utilities make full assessment impossible during the inspection window.

- Deferred maintenance: Peeling paint, rotted wood, broken windows, and water intrusion stains signal years of neglect. Each item compounds repair costs when left unaddressed.

- Environmental hazards: Asbestos, lead paint, and mold are common in older distressed properties and require licensed remediation, not standard contractor work.

Risk-adjusted repair numbers can exceed base estimates by 25–50% due to hidden liabilities when property access is limited or utilities are disconnected. This is the unknown repair reserve, and every distressed deal needs one built into the underwriting model.

Pro Tip: When you cannot access the full property or utilities are off, add a minimum 30% contingency buffer on top of your confirmed repair estimate. Treat it as a real cost, not a placeholder.

Physical inspections by experts reveal risks that financial data alone cannot capture. This is especially true for distressed property records that show code violations or permit history. A property with open permits or unresolved code violations carries legal liability that transfers to the buyer at closing.

Which financial and market factors shape calculating investment potential?

Calculating investment potential in distressed real estate goes beyond repair costs. The full financial picture includes acquisition price, financing costs, holding costs, selling costs, and any liens or back taxes attached to the title.

Here is the standard framework investors use to build a disciplined maximum offer:

- Start with ARV. This is your ceiling. Everything else works backward from here.

- Subtract total renovation costs. Use your PCA findings plus the unknown repair reserve.

- Subtract holding costs. Property taxes, insurance, utilities, and loan interest accumulate every month the property sits unsold. A six-month hold on a $300,000 renovation project can add $15,000 or more in carrying costs.

- Subtract selling costs. Agent commissions, closing costs, and transfer taxes typically run 8–10% of the sale price.

- Subtract your desired profit margin. This is non-negotiable. If the margin disappears before you reach this step, the deal does not work at the asking price.

- The result is your maximum allowable offer (MAO). Paying more than this number means you are subsidizing the seller’s problem with your own capital.

For multifamily distressed assets, the analysis adds another layer. Success relies on verifying actual rents versus scheduled rents and normalizing operating expenses. A 10-unit building showing $12,000 per month in scheduled rent may only collect $7,500 due to vacancies, non-paying tenants, and deferred lease renewals. Underwrite to actual cash flow, not the rent roll on paper.

Capital market conditions and underwriting assumptions shift faster in 2026 than in prior cycles. Interest rate changes affect both your financing costs and the buyer pool for your exit. A deal underwritten at 7% financing that closes at 8.5% can eliminate the entire profit margin on a thin deal.

Pro Tip: Always model your deal at two interest rate scenarios: your current rate and a rate 150 basis points higher. If the deal breaks at the higher rate, your margin is too thin.

Lien research is not optional. Back taxes, mechanic’s liens, and HOA judgments attach to the property and survive the sale unless cleared at closing. Underwriting must precede monetization decisions to reveal hidden leverage, equity, and realistic exit strategies. A title search and lien payoff analysis belong in week one of due diligence, not week four.

What common pitfalls should investors avoid with distressed properties?

Most distressed deal failures trace back to a short list of repeatable mistakes. Recognizing them before you make an offer is the difference between a profitable renovation and a capital loss.

- Anchoring to assessed value. Tax assessments lag the market by one to three years in most jurisdictions. Using them to justify an offer price is a valuation error, not a negotiation tactic.

- Ignoring the unknown repair reserve. When utilities are off or access is restricted, confirmed repair estimates are incomplete by definition. Investors who skip the reserve buffer routinely discover $40,000 in hidden damage after closing.

- Skipping title and lien review. Buying a distressed property with unresolved liens means inheriting the seller’s debt. This is not a negotiable risk. It is a deal-killer or a price reduction.

- Underestimating holding costs. A renovation that runs three months over schedule on a property with a $2,500 monthly carrying cost adds $7,500 to your cost basis. Model delays as a probability, not an exception.

- Treating ARV as guaranteed. The market moves. An ARV calculated in january may be outdated by april if comparable sales shift. Revalidate your comps before you close, not just before you make an offer.

Early versus late-stage distressed status dictates different investment strategies and valuation approaches. Early-stage distress offers flexibility to negotiate workout options and renovation timelines. Late-stage distress, such as a property already in foreclosure auction, prioritizes recovery speed over upside potential. Know which stage you are buying into before you build your model.

“Valuation in distressed real estate is not a one-time event. It is an ongoing risk management process that requires updates as market and property conditions evolve.” — BBG Real Estate Advisors

Valuation must adapt continuously as market and property conditions change post-acquisition. Investors who set their numbers at contract and never revisit them get caught by market shifts, cost overruns, and financing changes that were entirely predictable.

Pro Tip: Schedule a formal valuation review at three milestones: contract signing, midpoint of renovation, and 30 days before listing. Catching a problem at midpoint costs far less than discovering it at closing.

Key takeaways

Accurate distressed property valuation requires separating as-is condition from after-repaired potential, building in unknown repair reserves, and stress-testing every financial assumption against real market conditions.

| Point | Details |

|---|---|

| Differentiate As-Is from ARV | Never anchor your offer to assessed value. Use licensed appraisals and recent comps for both figures. |

| Build an unknown repair reserve | Add 25–50% above confirmed repair estimates when property access or utilities are limited. |

| Model all holding and selling costs | Include financing, taxes, insurance, agent fees, and lien payoffs before calculating your maximum offer. |

| Verify actual cash flow on multifamily | Underwrite to collected rents and normalized expenses, not the scheduled rent roll. |

| Update valuations throughout the deal | Revalidate ARV, repair costs, and financing assumptions at contract, midpoint, and pre-listing. |

What I’ve learned about distressed property valuation the hard way

The investors I’ve watched lose money on distressed deals almost always made the same mistake. They fell in love with the ARV and treated everything between the current condition and that exit number as a straight line. It never is.

The physical condition of a distressed property is not a fixed variable. It is a moving target that gets worse the longer the property sits vacant. A roof that looked manageable in october can be a full replacement by march after a hard winter. The unknown repair reserve is not a conservative accounting trick. It is a reflection of reality.

What I’ve also seen is that investors who find undervalued properties early before the competition arrives have more room to negotiate and more time to do thorough due diligence. The investors crowded around the same foreclosure auction list are playing a commoditized game with thin margins and no information edge.

The tools available in 2026 for tracking permit activity, code violations, and deferred maintenance signals give serious investors a real advantage. Use them. The market rewards the investor who acts on better information, not the one who moves fastest on the same data everyone else has.

— Avi

How Shovld helps you assess distressed real estate before the crowd does

Shovld tracks permits, code violations, HOA pressure, and deferred maintenance patterns across U.S. markets to surface distressed property opportunities before they hit public listings.

For investors who need to evaluate fixer-upper value with real data behind it, Shovld’s signal intelligence cuts the time between spotting an opportunity and building a credible underwriting model. The platform scores and verifies opportunities from public records so you are not starting from scratch on every deal. Knowing a property has accumulated code violations and deferred permit activity before you walk through the door changes the entire negotiation. See Shovld’s pricing plans to find the right fit for your market and deal volume. You can also learn more about what Shovld does and how the platform works for active investors.

FAQ

What is the difference between as-is value and ARV?

As-is value is what a distressed property is worth in its current condition. ARV is the projected market value after all planned repairs and renovations are complete. Your profit margin lives in the spread between these two numbers.

How do I calculate the maximum offer price for a distressed property?

Start with ARV, then subtract total renovation costs, unknown repair reserves, holding costs, selling costs, and your required profit margin. The result is your maximum allowable offer. Paying above this number means the deal does not pencil.

Why is assessed value unreliable for distressed property deals?

Assessed value is a government estimate used for tax purposes and typically lags actual market conditions by one to three years. It does not reflect current buyer demand, property condition, or recent comparable sales.

What is an unknown repair reserve and why does it matter?

An unknown repair reserve is a cost buffer added to your confirmed repair estimate to account for damage you cannot see due to limited access or disconnected utilities. Risk-adjusted repair numbers can exceed base estimates by 25–50% on distressed assets with restricted access.

How often should I update my valuation on a distressed property?

Valuation should be updated at three points: contract signing, midpoint of renovation, and 30 days before listing. Market shifts, cost overruns, and financing changes can all erode margins that looked solid at the start of the deal.