Foreclosure Timeline Knowledge: What Every Investor Needs

Foreclosure timeline knowledge is defined as a structured understanding of each legal stage a distressed property passes through, from the first missed payment to bank ownership, and why foreclosure timeline knowledge helps investors is simple: it turns a chaotic, high-stakes process into a predictable sequence you can plan around. Federal regulation requires lenders to wait 120 days of delinquency before starting formal foreclosure proceedings. That window alone creates a pre-foreclosure opportunity most investors miss because they only show up at the auction. State laws then layer additional variation on top, stretching timelines from two months to over two years depending on whether a court must approve each step. Investors who map these stages in advance stop gambling and start executing.

Why foreclosure timeline knowledge helps investors win deals early

The foreclosure process follows a predictable sequence, and each stage carries a different risk profile and a different opportunity. Understanding these stages turns what feels like an intimidating legal event into a manageable process with clear decision points.

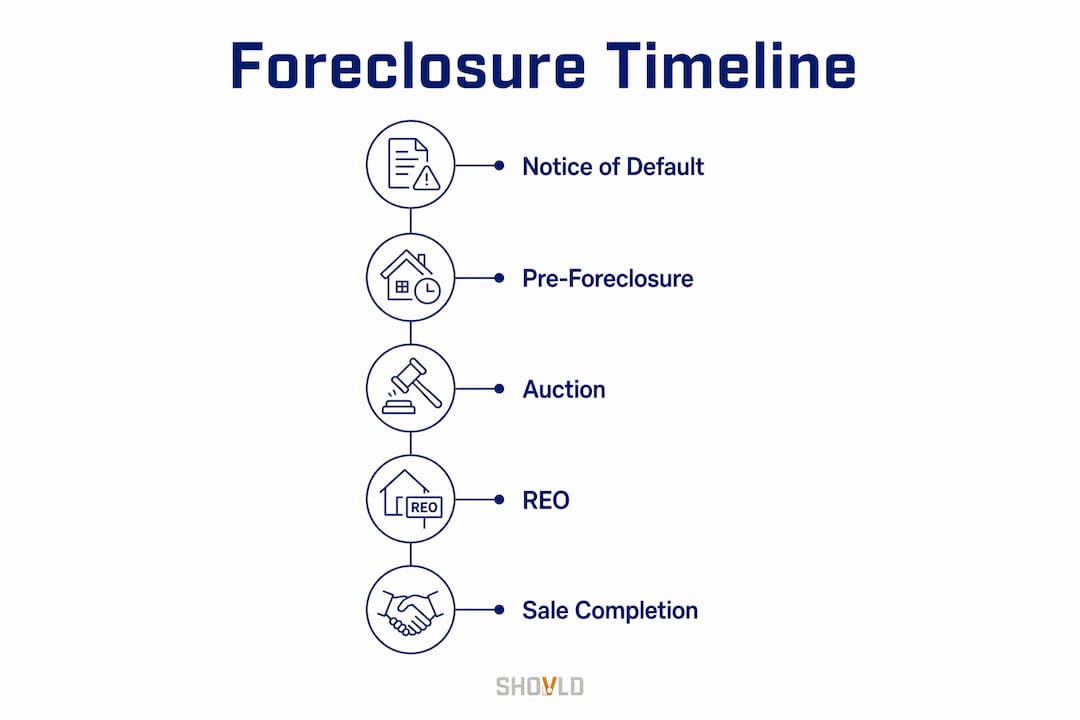

The five stages every investor must know

Missed payment. The borrower falls behind. Nothing is public yet, but the clock starts. Investors who track early delinquency signals can reach homeowners before any competitor does.

Notice of Default (NOD). The lender files a public notice, typically after 90 days of missed payments. This is the first public signal that a property is entering distress. It triggers the formal pre-foreclosure window.

Pre-foreclosure period. The homeowner still owns the property and can sell it. This stage offers the best negotiation access and the widest range of financing options. The 120-day delinquency rule means this window is federally protected and consistent across all 50 states.

Auction (Trustee Sale or Sheriff’s Sale). The property sells to the highest bidder, usually on the courthouse steps or online. Buyers typically must pay cash on the day of sale, and they acquire the property without an interior inspection.

REO (Real Estate Owned). If the property does not sell at auction, the lender takes ownership. The bank then lists it for sale, often at a discount, with clear title and the ability to finance conventionally.

Each stage compresses or expands your preparation time. Miss the NOD and you lose weeks of lead time. Show up unprepared at auction and you risk buying a property with unknown liens or structural damage.

Pro Tip: Set up public record alerts for Notice of Default filings in your target counties. Most county recorder websites offer free email notifications, and that single habit puts you ahead of investors who only track MLS listings.

The difference between judicial and non-judicial foreclosure procedures also reshapes your timeline. Judicial foreclosure states require court approval at each step, which extends the process and gives investors more preparation time. Non-judicial states move faster, which compresses due diligence windows but also means less competition at earlier stages.

How do state foreclosure timelines affect your investment strategy?

State law is the single biggest variable in foreclosure investing. Non-judicial foreclosures can close in as little as 2–6 months. Judicial foreclosures in states like New York or Florida can run 6 months to over 2 years. That gap is not just a scheduling inconvenience. It determines your financing approach, your due diligence depth, and your risk exposure.

Judicial vs. non-judicial states: what changes for you

In a non-judicial state like Texas or California, the process moves quickly once the NOD is filed. You have a narrow window to inspect, research title, and arrange financing. Traditional mortgage lenders cannot close fast enough for auction purchases. That reality pushes investors toward cash reserves or hard money lending, which carries higher interest costs but matches the timeline.

In a judicial state, the extended timeline is actually an asset for prepared investors. You have months to conduct a thorough title search, walk the property, and line up conventional financing. The tradeoff is that more investors also have time to find the deal, which increases competition at later stages.

State-mandated notice periods before auctions add another layer. Some states require 21 days of public notice before a sale. Others require 90 days. Knowing your state’s requirement tells you exactly when to start your due diligence clock.

Pro Tip: Before targeting a new market, pull the state’s foreclosure statute and note three numbers: the minimum delinquency period before NOD, the notice period before auction, and the redemption period after sale. Those three numbers define your entire investment timeline in that state.

Fast foreclosure timelines demand early due diligence, cash financing readiness, and quick decision making. Traditional lenders often cannot keep pace with short timelines, which is why investors in non-judicial states treat cash or hard money as a baseline requirement, not a backup plan.

Why does timeline mastery reduce risk and improve returns?

Reactive investing is the most common mistake in foreclosure markets. Investors who show up at auction without prior research are not investing. They are bidding on uncertainty. Successful investors verify title, estimate repairs, and walk away when the numbers do not work. Timeline knowledge is what makes that discipline possible.

Matching your strategy to the right stage is the core skill. Here is how stage alignment works in practice:

Pre-foreclosure. Best for investors who want negotiation access and flexible financing. The homeowner is motivated but not yet dispossessed. You can inspect the property, negotiate price, and use conventional or portfolio financing.

Auction. Best for experienced investors with cash reserves and deep market knowledge. You buy without interior access and must close immediately. The discount can be significant, but so can the unknowns.

REO. Best for newer investors. The bank has cleared the title, the property is vacant, and you can finance with a conventional loan. The discount is smaller, but the risk is lower.

Specializing by stage reduces risk and builds expertise. Beginners belong in REO. Intermediate investors can work pre-foreclosure. Experienced investors with cash and market depth can compete at auction. Jumping stages before you are ready is where most losses happen.

Title verification is non-negotiable at every stage. Foreclosed properties can carry unpaid tax liens, HOA judgments, or secondary mortgages that survive the sale. A title search before you commit protects you from inheriting debt that erases your margin. Knowing your timeline tells you exactly how much time you have to complete that search before you must act.

The emotional trap in foreclosure investing is real. Distressed properties often look like obvious deals, and the urgency of an auction deadline creates pressure to decide fast. Investors who understand the timeline resist that pressure because they have already done the work before the deadline arrives.

How can investors apply foreclosure timeline knowledge to source and close deals?

Practical application starts before the NOD is even filed. Investors who identify pre-foreclosure properties early reach homeowners during the period of maximum flexibility, before the property becomes public knowledge and competition increases.

Here is a repeatable process for applying timeline knowledge to every deal:

Track early signals. Monitor public records for NOD filings, tax delinquencies, and code violations in your target market. These signals appear weeks or months before a property hits any investor list.

Schedule due diligence immediately. Once you identify a pre-foreclosure property, book your title search and property walkthrough within the first week. Do not wait for the homeowner to respond before starting your research.

Match financing to the timeline. If the state moves fast, have cash or a hard money line ready before you need it. If the state is judicial, you may have time to arrange conventional financing, but confirm your lender’s closing timeline against the auction date.

Approach homeowners with empathy. Pre-foreclosure negotiations work best when investors acknowledge the homeowner’s situation honestly. Homeowners in distress respond to investors who offer a real solution, not just a low offer. That approach also builds a reputation that generates referrals.

Build a stage-specific checklist. Create separate checklists for pre-foreclosure, auction, and REO purchases. Each stage has different documentation requirements, financing needs, and risk factors. A single generic checklist creates gaps.

Use technology to automate alerts. Manual public record searches are slow and inconsistent. Platforms that track distressed property signals across multiple data sources give you earlier visibility and fewer missed opportunities.

Foreclosure activity also drives renovation demand, which means your timeline knowledge affects not just acquisition but also your contractor scheduling and repair cost estimates. Investors who plan renovation timelines alongside acquisition timelines avoid the costly gap between closing and rehab start.

Understanding foreclosure terminology and stages helps investors avoid costly mistakes and emotional decisions. Clear knowledge turns foreclosure from an intimidating event into a manageable process with defined steps and predictable outcomes.

Key takeaways

Foreclosure timeline knowledge is the foundation of disciplined distressed property investing, giving investors the structure to act early, prepare thoroughly, and match strategy to stage.

PointDetailsFederal 120-day ruleLenders cannot start foreclosure until 120 days of delinquency, creating a consistent pre-foreclosure window nationwide.State timeline variationNon-judicial states move in 2–6 months; judicial states can take 2+ years, which changes your financing and due diligence approach.Stage-matched strategyBeginners should target REO, intermediate investors pre-foreclosure, and experienced investors auctions, based on risk tolerance and cash readiness.Title verification is mandatoryEvery foreclosure stage carries lien risk; a title search before commitment protects your margin from inherited debt.Early signal trackingMonitoring NOD filings and tax delinquencies gives you access to deals before they become public and competitive.

What I’ve learned from watching investors get the timing wrong

Most investors who lose money in foreclosure markets do not lose it because they picked the wrong property. They lose it because they showed up at the wrong stage without the right preparation. I have watched experienced investors bid at auction on properties they had never walked, assuming the discount justified the unknown. It rarely does.

The investors who build real, repeatable returns treat the foreclosure timeline the way a contractor treats a project schedule. They know every deadline, they work backward from it, and they never let urgency replace preparation. That discipline is not natural. It has to be built through stage specialization and repetition.

My honest advice: pick one stage and master it before you move to the next. If you are newer to finding undervalued distressed properties, start with REO. The bank has done the title work, the property is vacant, and you can finance conventionally. The margin is thinner, but the education is cheaper. Once you understand how a deal moves from NOD to REO, you will recognize the pre-foreclosure opportunity with far more confidence.

Approaching pre-foreclosure deals with empathy also matters more than most investors admit. Homeowners in distress are not just motivated sellers. They are people in a difficult situation. Investors who lead with a genuine solution, not just a low number, close more deals and get more referrals. That reputation compounds over time in ways that no marketing budget can replicate.

— Avi

How Shovld gives investors an earlier view of distressed opportunities

Shovld tracks public record signals across U.S. markets, including NOD filings, tax delinquencies, code violations, and HOA pressure, and scores them into verified opportunities before they become crowded. Investors using Shovld see distressed properties earlier, which means more time for due diligence and better negotiation positioning.

The platform combines AI-powered lead scoring with workflow automation, so you spend less time searching records manually and more time evaluating deals that actually fit your stage and financing profile. Shovld’s signal intelligence plans are built for investors who want to act before the market reacts, not after the auction list goes public.

FAQ

What is the 120-day rule in foreclosure investing?

The 120-day delinquency rule requires lenders to wait at least 120 days after a borrower misses payments before starting formal foreclosure proceedings. This rule applies nationwide and creates a consistent pre-foreclosure window for investors.

How long does a foreclosure take from start to finish?

Foreclosure timelines range from 2–6 months in non-judicial states to 6 months or more than 2 years in judicial states. State law determines the process type and the length of each required notice period.

What is the safest foreclosure stage for new investors?

REO properties are the safest entry point for new investors because the bank has cleared the title, the property is vacant, and conventional financing is available. The discount is smaller than at auction, but the risk is significantly lower.

Why do foreclosure auctions require cash?

Auction purchases require immediate payment because the sale closes on the day of the bid, leaving no time for lender underwriting. Investors must arrive with certified funds or a pre-arranged hard money line to participate.

How does empathy improve pre-foreclosure negotiations?

Homeowners in pre-foreclosure are under significant financial and emotional stress. Investors who acknowledge that reality and present a clear, honest solution close more deals and build a referral reputation that generates future opportunities.