Why Tax Lien Properties Attract Investors: 2026 Guide

Tax lien investing is defined as purchasing government-issued certificates representing delinquent property taxes, earning statutory interest while the property owner retains the right to redeem the debt. This structure is why tax lien properties attract investors across every experience level: the returns are legally set, the collateral is real estate, and you never have to manage a tenant or fix a roof. The formal industry term is “tax lien certificate investing,” and understanding that distinction matters because it separates this asset class from direct property ownership entirely. Investors in states like Florida, Arizona, and Illinois have used this mechanism for decades to generate passive income with a defined risk profile.

How does tax lien investing work and generate returns?

The mechanics are straightforward. A county government places a lien on a property when the owner fails to pay property taxes. The county then auctions those lien rights to investors, who pay the delinquent tax balance and earn interest while the owner has a redemption period to pay them back.

The process follows a predictable sequence:

- County files the lien. The local government records the delinquency and schedules an auction, typically within 12 months of the missed payment.

- Investor purchases the certificate. You pay the delinquent tax amount at auction and receive a certificate entitling you to interest and fees.

- Redemption period begins. The property owner has a legally defined window, often one to three years depending on the state, to repay the investor the full amount plus accrued interest.

- Outcome: redemption or foreclosure. If the owner pays, you collect your principal plus interest. If they do not, you can initiate foreclosure proceedings and potentially acquire the property.

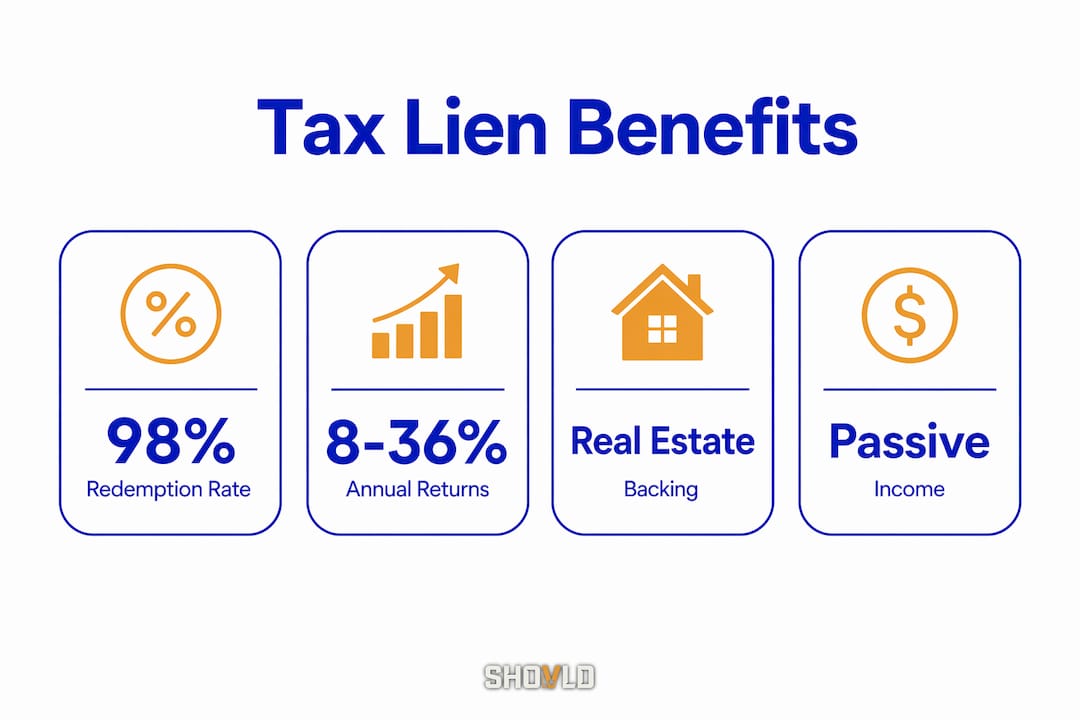

About 98% of property owners redeem their liens before foreclosure. That figure reframes the entire investment: tax lien certificates function primarily as structured income instruments, not property acquisition plays.

Pro Tip: Research the redemption history for a specific county before bidding. Counties with high redemption rates signal lower foreclosure risk and more predictable interest income.

What are the main benefits of investing in tax lien properties?

The benefits of tax lien investing are concrete and measurable, which is exactly why the asset class draws serious capital.

- High, state-set interest rates. Tax lien certificates pay 8%–36% annual interest depending on the state. Florida caps rates at 18%, while Illinois allows up to 36%. No stock dividend or savings account comes close to that ceiling.

- Real estate collateral. The lien is secured by the physical property. If the owner defaults completely, the investor holds a legal claim that can lead to property ownership through foreclosure.

- Passive income without property management. Tax liens eliminate tenant and maintenance overhead that burdens rental property investors. You hold a certificate, not a building.

- Portfolio diversification. Tax lien income does not correlate directly with equity market movements. When the stock market drops, property tax obligations in most counties remain unchanged.

- Increased accessibility. Counties increasingly run auctions online, meaning investors in 2026 can bid on certificates in multiple states from a single laptop without traveling to a courthouse.

The combination of high yields, real asset backing, and passive structure is rare in any investment category. That combination is the core of the attractiveness of tax lien properties for both new and experienced investors.

How do tax lien investments compare with tax deed investing?

Tax liens and tax deeds are related but fundamentally different instruments. Confusing them is one of the most common mistakes new investors make.

| Factor | Tax lien certificate | Tax deed |

|---|---|---|

| What you purchase | The right to collect debt plus interest | Direct ownership of the property |

| Return type | Fixed statutory interest rate | Profit from resale after repairs |

| Operational demand | Minimal: track redemption deadlines | High: repairs, title clearing, resale |

| Predictability | High: rate is set by state law | Low: depends on property condition and market |

| Risk profile | Lower: 98% redemption rate | Higher: property may need significant work |

| Entry cost | Typically lower | Typically higher |

Tax liens offer more predictable returns because the interest rate is fixed by state statute before you bid. Tax deeds require you to estimate repair costs, navigate title issues, and time a resale correctly. For investors who want income without operational complexity, tax liens win on nearly every dimension.

Tax deeds do offer one advantage: the potential for outsized gains if you acquire a property well below market value. But that upside comes with repair risk, holding costs, and market timing uncertainty that most income-focused investors prefer to avoid. Understanding tax delinquency’s role in off-market deals helps clarify where each instrument fits a broader investment strategy.

What practical strategies help identify good tax lien investment opportunities?

Identifying strong tax lien opportunities requires a disciplined, data-driven approach. The investors who consistently profit are not the ones chasing the highest interest rates. They are the ones who understand redemption probability before they bid.

- Prioritize redemption probability over property value. Most strategies succeed or fail based on redemption likelihood and deadline tracking. A lien on a property with a motivated owner and an active mortgage is far safer than a lien on a vacant lot with no lender interest.

- Research parcel-level data. Tracking parcel details and redemption windows is a core operational requirement. Know the property type, assessed value, existing encumbrances, and any prior lien history before committing capital.

- Understand auction mechanics. Bid-down interest rate auctions and premium bidding formats produce very different effective yields. In a bid-down state like Florida, competitive auctions can push the rate from 18% down to near zero. In a premium bidding state, you may pay more than the lien face value and risk losing that premium if the owner redeems.

- Avoid overbidding on low-value properties. A lien on a property worth $15,000 with $12,000 in delinquent taxes leaves almost no equity cushion if foreclosure becomes necessary.

- Track subsequent taxes during the hold period. Owners who miss one year of taxes often miss the next. Monitoring whether additional liens are accruing protects your position and signals whether redemption is still likely.

Pro Tip: Use county GIS portals and public record databases to cross-reference parcel data before every auction. Investors who skip this step are the ones who end up holding liens on properties with environmental issues or title defects.

The investors who treat tax lien investing as a research discipline rather than a passive bet consistently outperform those who rely on interest rate ceilings alone. Platforms that aggregate distressed property signals give you a meaningful edge in pre-auction due diligence.

Key takeaways

Tax lien certificate investing generates predictable, high-interest income secured by real estate, with approximately 98% of liens redeemed before foreclosure, making it a structured income strategy rather than a property acquisition play.

| Point | Details |

|---|---|

| High statutory returns | State-set rates range from 8%–36% annually, far exceeding most fixed-income alternatives. |

| Real estate collateral | Every certificate is backed by a physical property, giving investors a legal claim if the owner defaults. |

| Passive income structure | No tenant management or maintenance is required, unlike rental property ownership. |

| Redemption is the norm | About 98% of liens are redeemed, so interest income is the primary outcome for most investors. |

| Auction format matters | Bid-down and premium bidding formats directly affect effective yield and must be understood before bidding. |

Why tax liens still deserve a place in your portfolio in 2026

The case for tax lien investing has not weakened. If anything, the 2026 environment makes it more accessible than it has ever been. Online auctions have removed the geographic barrier that once limited participation to local investors willing to sit in a county courthouse. You can now build a multi-state certificate portfolio from a single platform.

What I find most underappreciated is the diversification argument. Most investors think about diversification in terms of asset classes: stocks, bonds, real estate. Tax liens sit at an unusual intersection. The income is tied to local property tax dynamics, not to corporate earnings or Federal Reserve rate decisions. That independence has real value in a portfolio that is already exposed to equity volatility.

The caution I would offer is about institutional competition. Large funds have entered the tax lien space in several high-volume counties, particularly in Florida and New Jersey. They bid aggressively and accept lower effective yields because of their scale. Individual investors competing in those markets are often playing a losing game. The better opportunity is in smaller counties and secondary markets where institutional capital has not crowded in yet. That is where the 36% ceiling is still achievable and where disciplined research creates a genuine edge.

The investors I respect in this space treat every certificate like a short-term loan underwriting decision. They ask: who is the borrower, what is the collateral, and what is the probability of repayment? That framing keeps them out of trouble and keeps their returns consistent.

— Avi

How Shovld helps investors find tax lien opportunities early

Shovld tracks public-record signals across U.S. markets, including tax delinquency indicators, code violations, and distressed-property patterns, giving investors early visibility before auctions get crowded.

For investors focused on tax lien certificate strategies, that early signal layer matters. Knowing which properties are accumulating delinquency signals before the county schedules an auction means you can research parcels thoroughly rather than scrambling at the last minute. Shovld scores and verifies those signals so you spend time on the best opportunities, not on dead ends. Investors who want to act before the market reacts can review Shovld’s plans and see how the platform fits their due diligence workflow. You can also learn what Shovld does and how its signal intelligence applies to real estate investment decisions.

FAQ

What is a tax lien certificate?

A tax lien certificate is a government-issued document representing the right to collect delinquent property taxes plus statutory interest. Investors purchase these certificates at county auctions and earn interest during the redemption period.

How much interest can tax lien investors earn?

Tax lien certificates pay 8%–36% annual interest depending on the state. The actual rate earned depends on auction format and competition at the time of bidding.

Do tax lien investors usually end up owning the property?

No. Approximately 98% of liens are redeemed by property owners before foreclosure, so most investors collect interest income rather than acquiring real estate.

What is the difference between a tax lien and a tax deed?

A tax lien gives you the right to collect debt plus interest. A tax deed transfers property ownership directly. Tax liens are more predictable; tax deeds carry higher operational and repair risk.

How do I find good tax lien investment opportunities?

Focus on redemption probability, parcel-level data, and auction format before bidding. Counties with high redemption rates and properties with active mortgages offer the most predictable returns. Platforms like Shovld that track distressed property indicators can surface early signals before auctions open.