Tax Delinquency’s Role in Off-Market Property Deals

Tax delinquency in real estate is defined as the failure to pay property taxes by the statutory due date, resulting in recorded tax liens that directly determine whether an off-market deal can close. The role of tax delinquency in off-market deals is more consequential than most investors anticipate. Unpaid taxes attach to the property as a senior lien, meaning they take legal priority over mortgages, private loans, and most other encumbrances. Title companies including Fidelity National Title and First American Title will not issue clean title insurance until every recorded tax lien is resolved. For investors sourcing deals outside the MLS, this legal reality shapes every stage of the transaction from initial offer through closing.

How tax liens and redemption periods create risk and opportunity

Tax liens are issued by local taxing authorities when property taxes go unpaid, and in many states those liens are then sold to private investors at public auctions. When an investor purchases a tax lien certificate, they effectively step into the role of a creditor. They earn statutory interest on the unpaid balance, and if the property owner fails to redeem the lien within the legally defined window, the certificate holder gains the right to initiate foreclosure proceedings.

That foreclosure right is what transforms tax delinquency from a legal headache into an off-market acquisition channel. The redemption period is the interval between lien issuance and the point at which a lien holder can foreclose. These windows vary significantly by state, and understanding them is the difference between a well-timed acquisition and a capital-intensive waiting game.

StateRedemption periodPenalty/interest rateNotesTexas180 days to 2 years25% to 50% premiumHomestead and agricultural properties get longer windowsGeorgia12 months20% premiumApplies to tax deed purchasersFlorida2 years18% max interestLien certificate state; competitive auctionIllinois2 to 3 years36% per 6 monthsExtended for owner-occupied propertiesCalifornia5 yearsVaries by countyTax deed state; no certificate system

The economics shift depending on whether the owner redeems or not. If the owner redeems, the investor collects the penalty return without ever taking title. If the owner does not redeem, the investor can foreclose and acquire the property, often well below market value. That dual outcome is what makes buying tax delinquent properties attractive to experienced investors who understand the legal timeline.

Key risks investors must account for during the redemption window:

Property condition can deteriorate with no legal right to enter or improve

Carrying costs accumulate while the outcome remains uncertain

Competing lien holders may complicate the foreclosure process

Environmental or structural issues discovered post-acquisition have no recourse

Pro Tip: Before bidding at a tax lien auction, pull the property’s full lien history from the county recorder’s office. A second IRS federal tax lien on the same property can survive a state tax lien foreclosure, leaving you with a title problem even after you win the auction.

Why tax delinquency complicates title clearance and closing

Title clearance is the single most common point of failure in off-market deals involving tax delinquent properties. Title insurers will not insure a property with an outstanding tax lien until the lien is paid off, formally released, or subordinated in writing. Without that release, no lender will fund a purchase loan, and cash buyers face unmarketable title if they ever try to resell or refinance.

The financial escalation compounds the problem. Missed property taxes trigger immediate penalties and fees, and those balances grow month over month. A $4,000 delinquency in year one can become a $7,500 obligation by the time a buyer negotiates a purchase, accounting for statutory penalties, interest, and county collection fees. That gap must be factored into the offer price or explicitly negotiated as a seller concession.

Federal tax liens issued by the IRS add another layer of complexity. IRS liens grow rapidly and carry strict post-lien remedies that are slower and more bureaucratic than state-level resolution. A federal lien requires a formal Certificate of Release or a Discharge of Property from the IRS, which can take 30 to 120 days to obtain. That timeline alone can kill a deal if it is not identified during initial due diligence.

Here is the standard sequence for resolving tax liens at closing in an off-market transaction:

Order a full title search from a licensed title company to identify all recorded liens, including municipal, state, and federal

Request a payoff statement from each taxing authority, confirming the exact amount needed for lien release

Negotiate with the seller on who absorbs the lien payoff, either through price reduction or seller-paid closing costs

Obtain written lien release documentation from each authority before or at closing

Confirm title insurer acceptance of all releases before funding

“Tax lien placement has priority over other liens and compresses seller options, accelerating off-market selling yet complicating buyer title assurance.” — TaxByCounty

Pro Tip: Budget an additional 30 to 90 days beyond your standard closing timeline whenever a property carries a recorded tax lien. Federal lien discharges and state redemption confirmations rarely move at the pace of a standard real estate transaction.

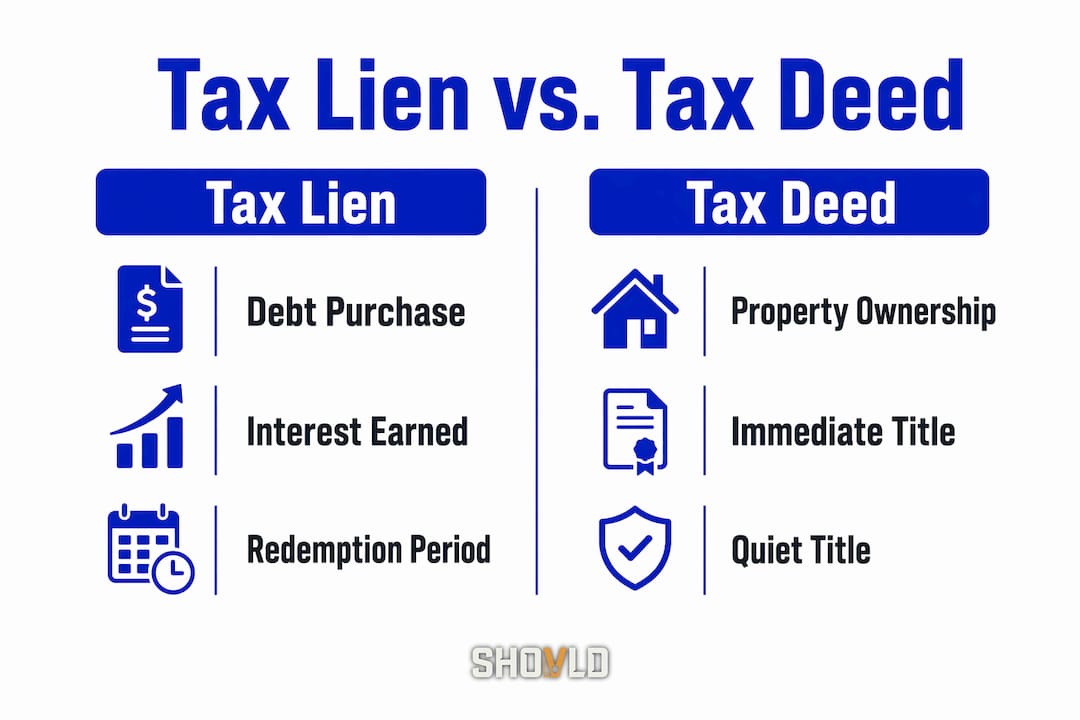

Tax lien vs. tax deed sales: what off-market investors need to know

The distinction between tax lien states and tax deed states is not semantic. It determines what you actually own after a tax sale, how long you wait to control the property, and what risks you carry.

In a tax lien state, the government sells the debt. The investor buys a certificate representing the unpaid taxes plus interest rights. The original owner retains possession and can redeem the property by paying the full amount owed. In a tax deed state, the government sells the property itself after the redemption period expires. The investor receives a deed, though title quality varies and quiet title actions are often necessary.

FeatureTax lien certificateTax deed saleWhat you purchaseThe debt obligationThe property itselfOwner possessionRetained during redemptionTransferred at saleRedemption rightsYes, during statutory windowVaries by stateTitle qualityRequires foreclosure for deedDeed issued, may need quiet titleInvestor controlLimited until foreclosureImmediate or near-immediateTypical return if redeemed8% to 36% interest/penaltyN/APrimary riskOwner redeems, no property acquiredTitle defects, unknown encumbrances

Tax deed sales carry the higher upside but also the greater exposure. Properties sold at tax deed auctions frequently have deferred maintenance, unknown occupants, or secondary liens that survived the sale process. Tax deed sales transfer ownership immediately or after the redemption period, but the deed quality is not equivalent to a warranty deed from a traditional sale.

Key considerations when choosing between lien and deed strategies:

Tax lien certificates suit investors who want predictable returns without property management exposure

Tax deed purchases suit investors prepared to take physical possession and manage rehabilitation

Hybrid strategies exist where investors buy liens with the intent to foreclose and acquire the deed

Pro Tip: In tax deed states, always run a quiet title action before listing or refinancing a property acquired through a tax sale. Title insurers in states like Georgia and Florida routinely require it, and skipping this step can freeze your exit strategy for months.

Strategies for navigating tax delinquency in off-market deals

Sourcing and closing tax delinquent properties off-market requires a system, not just a checklist. The investors who consistently profit from real estate tax delinquency are the ones who identify distress signals early, before the property reaches a public auction or attracts competing buyers.

The timing problem in off-market deal flow is real. Most investors enter the picture after a property has already been listed at a tax sale, at which point they are competing with dozens of other bidders and the discount has narrowed. The opportunity window is widest in the months before a tax sale, when the owner is under pressure but the property has not yet attracted public attention.

Practical steps for building a tax delinquency pipeline:

Pull delinquent tax rolls from county tax assessor websites, which are public record in most states

Cross-reference delinquent properties against code violation databases and permit records to identify compounding distress

Contact owners directly with a written offer before the tax sale date, framing the conversation around lien resolution as a mutual benefit

Work with a title company experienced in distressed property transactions to run preliminary title searches before making offers

Use signal intelligence platforms like Shovld to track multiple distress indicators across markets simultaneously, catching opportunities before they become crowded

Due diligence on a tax delinquent property must go beyond the lien itself. Verify the full lien stack, confirm the redemption period status, check for IRS liens separately from county records, and assess the property’s physical condition before committing to a price. Properties with undervalued characteristics needing work often carry deferred maintenance that compounds the cost of lien resolution.

Negotiation leverage shifts dramatically based on timing. An owner facing a tax sale in 60 days is far more motivated than one with 18 months remaining on the redemption clock. Knowing exactly where a property sits in the delinquency timeline is the single most valuable piece of information in any off-market negotiation involving unpaid taxes.

Key takeaways

Tax delinquency creates both the legal obstacle and the acquisition opportunity in off-market deals, and investors who master lien resolution, redemption timelines, and title clearance consistently outperform those who avoid distressed properties entirely.

PointDetailsTax liens block clean titleTitle insurers require full lien payoff or release before any transaction can close.Redemption periods define timingState-specific windows from 180 days to 5 years determine when investors can act or must wait.Lien vs. deed states differ fundamentallyTax lien certificates earn interest; tax deed sales transfer property with varying title quality.Federal liens require separate resolutionIRS Certificates of Release take 30 to 120 days and must be tracked independently of county records.Early identification wins the dealContacting owners before the public tax sale date maximizes negotiating leverage and minimizes competition.

What I’ve learned from watching investors get this wrong

Most investors who struggle with tax delinquent properties are not making analytical errors. They are making timing errors. They find the property after the tax sale has been scheduled, rush the due diligence, and underestimate the lien resolution timeline. Then they either overpay to close fast or lose the deal entirely when the title company flags a federal lien nobody caught.

The investors I have seen succeed in this space treat tax delinquency data the same way a trader treats market signals. They are not reacting to what is already public. They are watching for the early indicators: a property that has missed two consecutive tax payments, a code violation filed six months after the last permit, an owner who has stopped responding to municipal notices. Those signals, taken together, tell you a motivated seller is coming before that seller knows it themselves.

The other mistake I see constantly is treating all tax liens as equivalent. A $3,000 county lien on a $400,000 property in a tax lien state with a 12-month redemption period is a completely different risk profile than a $45,000 IRS lien on a $200,000 property in a tax deed state. The math, the timeline, and the legal process are entirely different. Investors who lump them together make offers that are either too low to get accepted or too high to generate a return.

My honest advice: build relationships with two or three title officers who specialize in distressed transactions. They will tell you things about a property’s lien history that no database will surface. That relationship is worth more than any software subscription in the early stages of building a tax delinquency strategy.

— Avi

How Shovld helps you find tax delinquent deals before the competition does

Off-market real estate strategy lives and dies on early visibility. Shovld tracks public-record signals including code violations, deferred maintenance patterns, permit gaps, and municipal records across multiple U.S. markets, scoring properties by distress level before they appear on any auction list.

For investors focused on tax delinquent properties, Shovld surfaces the compounding signals that indicate a motivated seller is approaching a decision point. That means you are making contact weeks or months before the tax sale date, when your offer carries real weight. Explore Shovld’s platform features to see how signal intelligence applies to your market, or review current pricing plans to find the right fit for your deal volume.

FAQ

What is the role of tax delinquency in off-market deals?

Tax delinquency creates recorded tax liens that block clean title, which forces sellers into motivated positions and opens off-market acquisition opportunities for investors who understand lien resolution and redemption timelines.

Can you buy a property with a tax lien attached?

Yes, but the lien must be paid off or formally released before title insurance can be issued and the transaction can close. In most off-market deals, the lien payoff is negotiated as part of the purchase price or handled at closing.

What is the difference between a tax lien and a tax deed sale?

A tax lien sale transfers the debt to an investor who earns interest and can foreclose after the redemption period. A tax deed sale transfers the property itself, giving the buyer more immediate control but often with lower title quality.

How long does it take to resolve a tax lien before closing?

State and county tax liens can often be resolved within days of payoff confirmation. Federal IRS liens require a formal Certificate of Release, which typically takes 30 to 120 days and must be planned for well in advance of the closing date.

How do I find tax delinquent properties for off-market deals?

County tax assessor websites publish delinquent tax rolls as public record in most states. Cross-referencing those records with code violations and permit data, or using a signal platform like Shovld, identifies the highest-distress properties before they reach public auction.