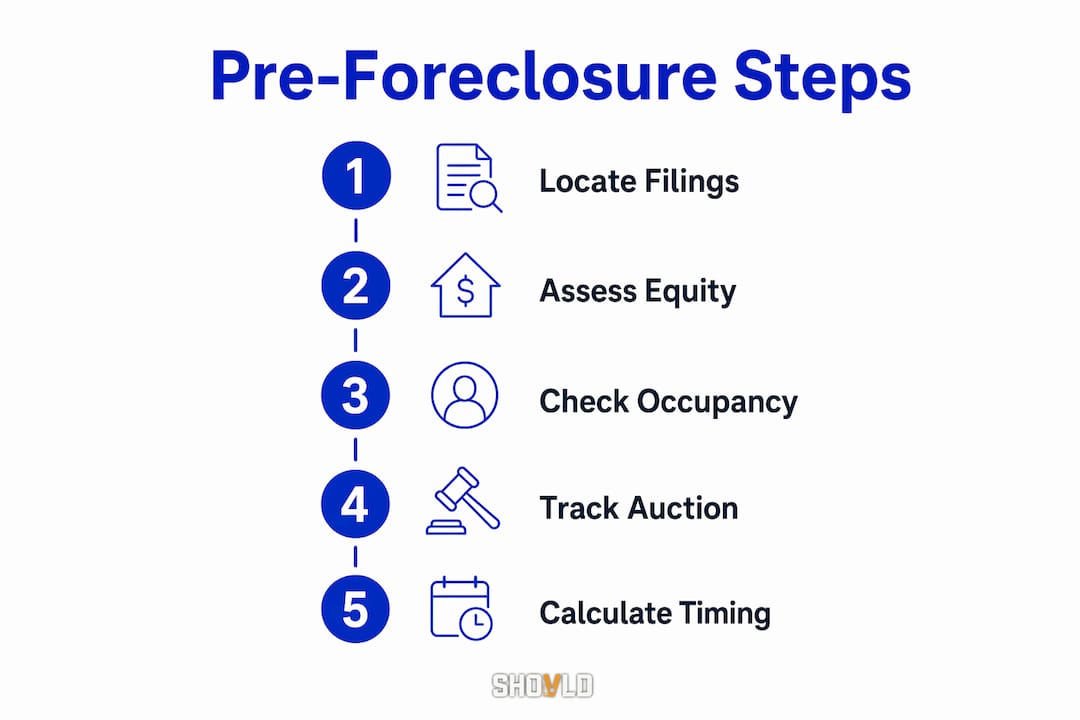

How to Identify Pre-Foreclosure Properties Early

Pre-foreclosure is the period between a lender’s first legal filing against a delinquent borrower and the actual auction date, and it represents the most underutilized window in real estate investing. To identify pre-foreclosure properties early, you need direct access to county public records, specifically Notices of Default (NODs), Lis Pendens filings, and Notices of Sale, before those signals reach aggregated platforms. Investors who act inside this window face less competition, negotiate with motivated sellers, and often secure properties at meaningful discounts. The off-market advantage is real, but only for those who move before the crowd.

How to identify pre-foreclosure properties early using public records

The most direct path to pre-foreclosure filings runs through your county recorder’s office. NODs, Lis Pendens documents, and Notices of Sale are all public record, and many counties now offer digital access through their official websites or third-party portals. These filings can appear days or weeks before auction, which gives you a genuine head start over buyers relying on MLS listings or popular consumer sites.

What you are looking for depends on the state. In judicial foreclosure states such as New York, Florida, and Illinois, the process runs through the courts, and a Lis Pendens is the first public signal. In non-judicial states such as California and Texas, an NOD triggers the clock. Knowing which document to track in your target market is not optional. It determines your entire sourcing strategy.

Beyond the county recorder, legal newspapers still publish foreclosure notices in many jurisdictions, and these are often overlooked by investors focused purely on digital sources. Real estate platforms like Zillow and Realtor.com surface some pre-foreclosure listings, but their data lags behind raw public records by days or weeks. For the sharpest early visibility, raw county data beats aggregated feeds every time.

County recorder’s office: Search by filing type (NOD, Lis Pendens, Notice of Sale) and filter by recent filing dates

Legal newspapers: Published notices often appear before digital databases update

State court portals: Judicial states publish Lis Pendens filings through court record systems

Specialized platforms: Services like ATTOM Data, PropertyRadar, and RealtyTrac aggregate and filter pre-foreclosure data by geography and filing date

Real estate agents: Agents with courthouse relationships or data subscriptions can surface off-market leads that never appear on MLS

Pro Tip: Set a recurring calendar alert to check your county recorder’s digital portal every Monday morning. New filings from the prior week are typically processed over the weekend, and Monday access puts you ahead of investors who check less frequently.

How to evaluate which pre-foreclosure properties are worth pursuing

Finding a filing is step one. Knowing whether it represents a real opportunity is step two, and most investors skip it. Calculating equity means comparing the outstanding mortgage balance against the property’s current market value. A property worth $350,000 with $180,000 owed is a strong candidate for a discounted cash purchase. A property worth $300,000 with $310,000 owed requires lender approval for a short sale, which adds complexity, time, and uncertainty.

Owner occupancy status matters almost as much as equity. An owner-occupied property signals a homeowner under personal financial stress, which typically means higher motivation to sell quickly and avoid foreclosure’s credit consequences. Vacant properties may indicate the owner has already walked away, which changes your negotiation dynamic entirely. Tax delinquency records, available through the county assessor’s office, add another urgency layer. A homeowner behind on both mortgage and property taxes is under compounded pressure and often more receptive to a fast solution.

IndicatorWhat it signalsPriority levelPositive equity (20%+)Discounted sale feasible without lender involvementHighUnderwater mortgageShort sale required; lender approval neededLow to mediumOwner-occupied statusHigh seller motivation; personal stakes involvedHighTax delinquencyCompounded financial pressure; urgency elevatedHighAuction date within 30 daysExpedited cash closing requiredSituational

Auction dates must be tracked carefully because they define your closing window. A property with 90 days to auction allows for standard due diligence. A property with 14 days requires a cash buyer ready to close fast or the deal collapses. Seasoned investors verify owner equity before outreach to avoid spending time and money on leads that cannot close without a lender’s cooperation.

Pro Tip: Pull the property’s mortgage origination date and original loan amount from public records, then apply a standard amortization schedule to estimate the current balance. It takes five minutes and tells you whether the equity math works before you spend a dollar on outreach.

What outreach methods actually work with pre-foreclosure homeowners

Reaching a homeowner in pre-foreclosure requires a different approach than standard investor marketing. These are people under financial and emotional stress, often receiving multiple solicitations simultaneously. Contacting homeowners within two weeks of the initial filing consistently yields higher response rates, before the wave of generic mailers and cold calls arrives and the owner shuts down.

The most effective outreach methods, ranked by engagement quality:

Personalized direct mail: A handwritten or personally addressed letter referencing the specific property and offering a clear, empathetic solution outperforms bulk mailers by a significant margin. Mention the filing by name only if it builds trust, not to intimidate.

Cold calling: A brief, respectful call focused on understanding the homeowner’s situation before pitching anything creates more goodwill than a scripted sales pitch. Ask questions. Listen first.

Text messaging: Short, non-aggressive texts work well for initial contact in markets where homeowners are younger or more digitally active. Keep the first message under 160 characters and include a clear opt-out.

Door knocking: The highest-effort method, but also the highest-trust builder. A face-to-face conversation with a calm, professional demeanor can open doors that mail and phone cannot.

Referral networks: Title companies, real estate attorneys, and bankruptcy attorneys often know about distressed properties before public filings appear. Building these relationships creates a pre-pipeline.

Owners in pre-foreclosure respond better to messaging that explains concrete benefits: avoiding a foreclosure on their credit report, receiving cash quickly, and moving on without the stress of a traditional sale. Generic “we buy houses” language signals mass marketing and gets ignored. Specificity and empathy are the differentiators.

Pro Tip: Reference a specific detail about the property or neighborhood in your first contact. It signals that you are a serious buyer, not a list-blaster, and it dramatically increases the chance of a callback.

Manual research vs. platforms: which approach finds distressed properties faster

The honest answer is that neither approach alone is optimal. Manual county record searches give you the freshest data and the deepest local knowledge, but they consume hours per week and do not scale across multiple markets. Aggregated foreclosure platforms update weekly and save significant time, but their data is always slightly behind raw filings and often shared with thousands of other subscribers.

The timing variable is the critical factor. In non-judicial states like California or Texas, the pre-foreclosure window can be as short as 60 to 90 days from filing to auction. In judicial states, the timeline often stretches to 180 days or more. That difference determines how much you can rely on weekly-updated platforms versus daily manual checks. In a 60-day market, a platform that updates every seven days has already consumed more than 10% of your available window before you see the lead.

Platforms like ATTOM Data Solutions, PropertyRadar, and RealtyTrac offer filtering by county, filing date, equity range, and owner status. These tools work well for building initial lead lists and monitoring large geographies. The gap they leave is the first 48 to 72 hours after a filing, which is precisely where the competitive advantage lives. Combining a daily county portal check for your core market with a platform subscription for broader coverage gives you both speed and scale.

State foreclosure timelines require tailored strategies, and investors who treat all markets the same consistently miss the best leads. Understanding early distress signals before a formal filing even appears is the next level of competitive advantage, one that pure foreclosure-data platforms do not provide.

Key takeaways

Identifying pre-foreclosure properties early requires combining raw public record access with disciplined equity analysis and timed, empathetic outreach before the market reacts.

PointDetailsPublic records are the primary sourceNODs, Lis Pendens, and Notices of Sale at county recorders’ offices provide the earliest signals.State timelines dictate urgencyNon-judicial states like California allow as little as 60 days; judicial states often allow 180 or more.Equity analysis filters real opportunitiesCompare mortgage balance to market value before outreach to avoid unworkable short-sale situations.First two weeks of filing are criticalContacting homeowners within this window yields higher response rates before competitor saturation.Platforms supplement but do not replace manual checksAggregated tools save time but lag behind raw county data by days, which matters in fast-moving markets.

Why timing is the only edge that actually holds

I have watched investors build elaborate outreach systems, subscribe to every data platform available, and still lose deals because they were three days late. The pre-foreclosure window is not forgiving, and the investors who consistently close deals are not necessarily the best negotiators. They are the ones who show up first.

The mistake I see most often is treating pre-foreclosure as a lead type rather than a timing problem. You can have the best script, the best offer, and the best financing, and still lose to someone who knocked on the door a week earlier. State-specific timeline knowledge is not a nice-to-have. In a non-judicial state, not knowing that you have 60 days instead of 180 means you are already behind before you start.

Equity analysis is where I see the second-biggest waste of resources. Investors contact every filing without checking whether the math works, then wonder why their close rate is low. Screening for positive equity before any outreach cuts your contact list significantly, but it also means every conversation you have is with a homeowner where a deal is actually possible. That shift alone changes your close rate more than any script improvement.

The empathy piece is real, but it is also misunderstood. Empathy in this context does not mean being soft. It means understanding that the homeowner’s primary fear is credit damage and loss of control, and addressing those fears directly in your first contact. That is not a soft skill. It is a conversion strategy.

— Avi

How Shovld helps you act before the market does

Shovld tracks public-record signals across multiple U.S. markets, including NODs, code violations, tax delinquency patterns, and deferred maintenance indicators, and surfaces them as scored, verified opportunities before they reach crowded platforms.

For real estate investors focused on finding distressed properties before the competition, Shovld’s signal intelligence removes the manual monitoring burden and delivers leads with context: equity estimates, owner status, filing dates, and urgency scores. You spend time on outreach, not on data collection. Explore Shovld’s pricing plans to see which coverage tier fits your target markets, or learn more about how Shovld works as a pre-foreclosure intelligence platform.

FAQ

What is pre-foreclosure and when does it start?

Pre-foreclosure begins when a lender files a Notice of Default or Lis Pendens against a delinquent borrower, signaling the start of the legal foreclosure process. This period ends at the auction date and represents the window where investors can negotiate directly with the homeowner.

How do I find pre-foreclosure homes before they hit the market?

Access your county recorder’s office directly, either in person or through its digital portal, to search for recent NOD and Lis Pendens filings. Specialized platforms like ATTOM Data Solutions and PropertyRadar also aggregate this data, though they typically lag raw county records by several days.

How long is the pre-foreclosure window?

The timeline varies significantly by state. Non-judicial states like California and Texas can move from filing to auction in as little as 60 to 90 days, while judicial states often take 180 days or longer, giving investors considerably more time to act.

What are the early signs of pre-foreclosure on a property?

The clearest early signs are public filings: a Notice of Default, a Lis Pendens, or a Notice of Sale recorded at the county level. Secondary indicators include tax delinquency records, code violations, and visible deferred maintenance, all of which can appear before a formal filing.

Should I contact a homeowner in pre-foreclosure directly?

Direct contact is both legal and effective when done respectfully. Reaching out within the first two weeks of a filing, before the homeowner is overwhelmed with solicitations, and focusing your message on concrete benefits like credit protection and a fast close produces the strongest response rates.